NBFC/MFI Company

NBFC/MFI Company

In India, the most common type of "legal structure" is a private limited company. A Private Limited Company Registration in India is governed by the Ministry of Corporate Affairs and is incorporated under the Companies Act of 2013. It is legally distinct from its owners. It is widely used because it provides numerous benefits to its directors, such as limited liability, which means that if the company defaults, bank/creditors can only sell the company's assets and not the directors' personal assets. Starting a business in India is a pipe dream unless you have a proper business entity to back it up.

Everyone, from veterans to novices, from budding start-ups to established entrepreneurs, and from north to south India, regard it as the best business entity. You can use our services to register your Private Limited Company. We have served clients from major cities throughout India for Private Limited Company Registration.

Advantages of NBFC License

Legal Separate Identity

Once an entity is registered it is born in the eyes of law which means it is separate from its owners, Directors, Managers, shareholders and employees etc.

Limited Liability

The liability of the Members is limited to the extent of Capital invested by them in the Company and therefore, they cannot be held personally liable for the debt and obligations of the Company.

Less Compliance

Registration of NBFC is pretty much easier than that of obtaining the license for Banks and there are less stringent regulations and cumbersome paperwork as compared to banks.

Low Interest Rate

The Rate of interest is the main considerations while applying for any type of loan. NBFCS interest rates lower to the bank rates. Thus, it is easier for the borrowers to afford them.

Lower Rules and Regulations

Less Rules and regulations are involved l.e which are prescribed under Companies Act, 2013 that to the banks. It makes the loan process less complicated and also helps the borrower to get loan easily.

Low Level of Cost

It involves cheaper cost and thereby are more profitable than banks. There are many rules and regulations to be followed in case of banks as compared to NBFCs.

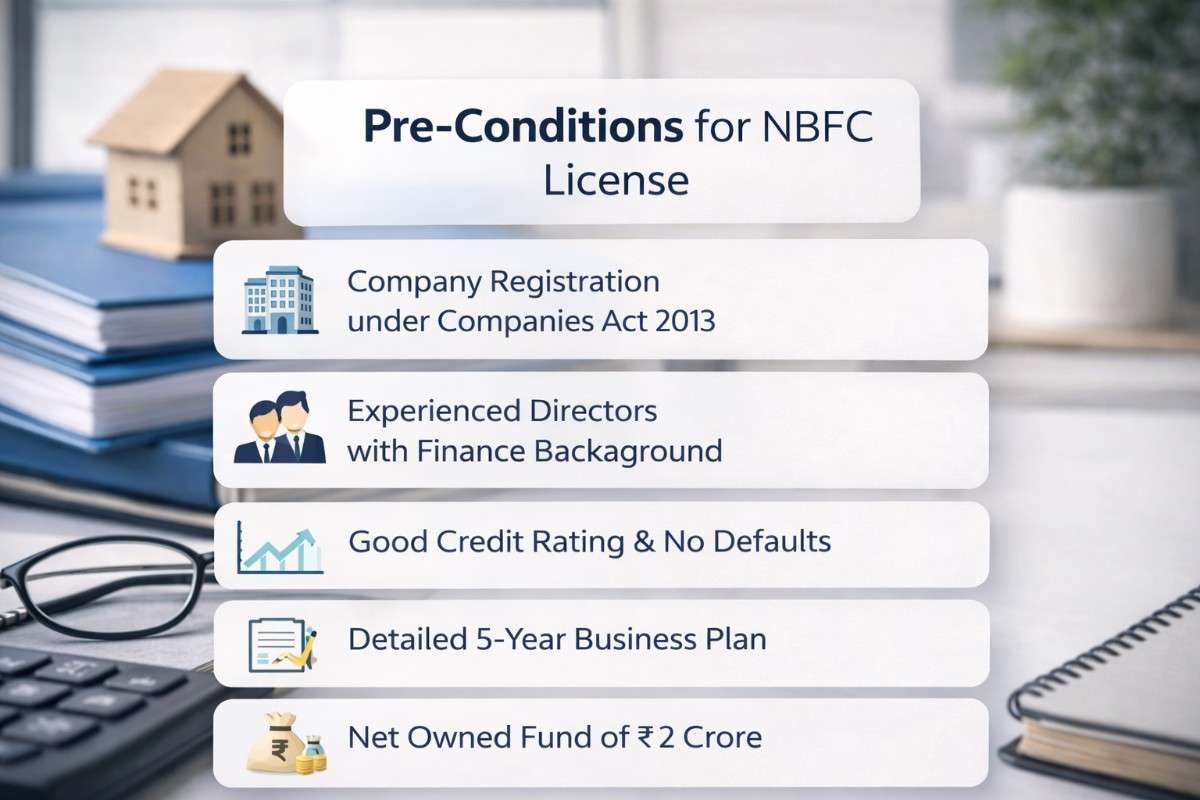

Pre-Conditions for NBFC License

- Company Registration Documents Complete Set of Documents of the Company i.e, COI, MOA, AOA, PAN Card, GST Certificate.

- Documents/Details of Directors and Members Brief Profile, Income proof, Credit rating report, Net-worth Certificate, Educational Qualification Certificates, Experience Certificates

- Documents of Company Bank Account Details stating the minimum NOF requirement, Banker's Report confirming that No Lien is remark on the Initial Fixed Deposit of Rs 2 crore, Board Resolution for approving the formation of NBFC, Detailed action plan for the next 5-years, Income Tax Returns.

NBFC / MFI Company Registration Criteria

As per Section 45-IA of Reserve Bank of India Act, 1934, the following conditions must be fulfilled in order to register a company as an NBFC:

The financial institution must be registered under Section 3 of the Companies Act 2013 or any other law for the time being in force;

It should have full time Directors and 1/3 of them must have minimum 10 years of experience in finance;

The credit rating of the Company must be good along with its Directors and they must not have any write offs or willfully defaulted on the repayment of loans to NBFC/Bank.

A unique detailed plan should be there stating the operations for the next 5 years;

The Company should comply with the FEMA Act, 1999

The Company should have Net Owned Fund of at least Rs. 2 Crore comprising of only equity paid-up share capital including the premium on shares & reserves, if any, (Preference share capital is not to be included). The minimum requirement of NOF differs for specialized NBFCs (NBFC-MFIs, NBFC Factors, and CICs).

Principal Business of a NBFC

The principal business of NBFC is to provide financial aid involving the lending, investments shares, stocks, debentures, bonds, leasing, hire-purchase, financial information service provider (NBFC-AA) insurance business, P2P Market Place lending business, chit business which are involved in the receiving of deposits under any scheme of arrangement. Despite of this, any of the following conditions must also be fulfilled in order to continue NBFC License:

Total Assets comprises more than 50% financial assets

More than 50% of the gross income should be generated from financial assets

Restricted Activities by NBFC

Agriculture Activities

Agriculture Activities

Purchase / Sale of Goods and Services

Purchase / Sale of construction of immovable property

Conditions by RBI for granting NBFC License

For Registration a company shall apply in the format as prescribed by the RBI. Before registration the company as NBFC, RBI has power to inspect the financial & other books in order to satisfy the following conditions:

That the NBFC should be able to pay its present as well as/or future investors in full as and when their claims accrue;

The management and the Board general character shall not be prejudicial to the interest of the public or its depositors;

It has sufficient capital structure and earning potential;

Public interest shall be served by licensing as an NBFC;

The grant of CoR shall not be unfavorable to the operation of the financial sector. And is consistent with monetary stability, economic growth and considering such other relevant policies of RBI.

Introduction of Micro-Finance Company

Micro finance Company refers to an array of financial services to low income group by providing loans, savings and insurance. Such funds are made available to poor entrepreneurs and small business owners who do not have any collateral and have no access to banking facilities. The people in rural areas need credit which is cheap and does not increase the burden in their input cost which is important so that these sectors grow and develop and raise the Indian economy.

Micro-finance companies can provide loans up to INR 50,000 in the rural area to various households, small businessmen and up to INR 1,25,000 to small entrepreneurs, enterprises and people in the urban areas for residential dwelling. Micro-finance Institutions generally provide loans without any collateral security to the small businessman, farmers, agriculturists, etc.. Such institutions are helping in rural and agricultural development and employment generation and boosting up the Indian Economy.

Microfinance can be registered in 2 ways; one as a non-profit organisation which is registered as Section-8 Company which doesn’t require any RBI approval and the other as Non-Banking.

Free Consultation

NBFC vs Bank Comparison

Understand the major differences between NBFCs and Banks.

| S:No | Particulars | NBFC | Bank |

|---|---|---|---|

| 1. | Governed | Companies Act, 2013 and sometimes RBI Act, 1934 | RBI Act, 1934 |

| 2. | Demand Deposits | It cannot accept Demand Deposits | It cannot accept Demand Deposits |

| 3. | Deposit Insurance | No Deposit Insurance is covered | It is covered under RBI's deposit Insurance |

| 4. | Payment and Settlement system of the RBI | It Cannot avail the payment and settlement system of RBI | Banks are provided the support of the Payment and Settlement System (RTGS, NEFT etc.,) |

| 5. | Foreign investment | It is allowed upto 100% | It is allowed upto 74% |

| 6. | Cash Reserve Ratio | Not Applicable | Applicable |

| 7. | Statutory Liquidity Ratio | 15% CRAR for Deposit taking NBFCs and Non-Deposit taking-Systemically Important NBFCs | Applicable |

Financial Company – Micro Finance Institution (NBFC-MFI) which can be formed by taking approval from the RBI.

Generation of Employment

The Microfinance companies offer loans to small entrepreneurs in rural areas which help them to start their own business which in turn will help in generation of employment in the country.

Collateral free Borrowings

Microfinance companies are eligible to provide borrowings to lower income groups of people without any collateral or margin money. It is beneficial for the people who cannot access the banks for loans.

Strengthening of Financial Condition

People in rural areas are dependent on daily wages, it is not possible for them to have employment during the whole year which creates hassles in their daily life. Such loans can strengthen the financial condition for a limited period of time.

Encourages entrepreneurship

Providing loans to low income groups without any collateral and margin money gives help to the entrepreneurs who want to establish any small business or shops nearby so that they can have recurring income.

Ideal for loans

For doing finance business

Simple & Secure Online Process

Dedicated Professional

Get Registration in 10-15 Days

Get Post Incorporation Assistance

Advantages of Micro Finance Company

Types of Micro-Finance Company NBFC-MFI

Non-Banking Financial Company – Micro Finance Institution (NBFC-MFI) NBFC-MFI is a non-deposit taking NBFC which can be setup with minimum net owned funds of Rs. 5 crore and having not less than 85% of its assets in the nature of qualifying assets. The conditions and limitations of the loans are as follows:

- Loan disbursed by an NBFC-MFI to a borrower with a rural household annual income not exceeding ₹ 1,25,000 or urban and semi-urban household income not exceeding ₹ 2,00,000;

- Loan amount should not exceed ₹ 75,000 in the first cycle and ₹ 1,25,000 in subsequent cycles;

- Total indebtedness of the borrower should not exceed ₹ 1,25,000;

- Tenure of the loan should not be less than 24 months for loan amount in excess of ₹15,000 with prepayment without penalty;

- Loan can be extended without collateral;

- Aggregate amount of loans, given for income generation, should not be less than 50 per cent of the total loans given by the MFIs;

- Loan can be repaid on weekly, fortnightly or monthly installments at the choice of the borrower