GST Annual Return

GST Annual Return

Form GSTR 9 is an GST annual return to be filed once in a year by the registered taxpayers under GST including those registered under the composition scheme. It consists of details regarding the supplies made and received during the year under different tax heads i.e. CGST, SGST and IGST. It consolidates the information furnished in the monthly/quarterly returns during the year.

GSTR 9 is an annual return to be filed yearly by taxpayers registered under GST.

It contains details concerning the outward and inward supplies made/received during the relevant previous year under various tax heads i.e. CGST, SGST & IGST, and HSN codes.

It is a consolidation of all the monthly/quarterly returns (GSTR-1, GSTR-2A, GSTR-3B) filed in that year. However complicated, this return assists in the extensive reconciliation of data for 100% transparent disclosures.

Who has to file GSTR 9?

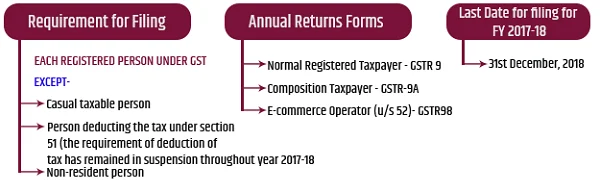

All the registered taxable persons under GST must file GSTR 9. However, following persons are not required to file GSTR 9

- Casual Taxable Person

- Input service distributors

- Non-resident taxable persons.

SUB-CATEGORIES UNDER GSTR-9

There are 4 sub-categories under GSTR-9 viz. GSTR-9, GSTR-9A, GSTR-9B, GSTR-9C. As we have already covered about GSTR-9 in the introduction, let’s jump straight to its sub-categories.

GSTR 9A: It was a simplified GST annual return introduced for all the business owners who opted for the composition scheme under the GST regime. This return included all the quarterly returns filed by the compounding dealers in that financial year. However, the return has been scrapped since FY 2019-20. Now there’s a change in filing frequency of Form GSTR 4 from Quarterly to Annual GSTR 4 (Annual) for Composite Taxpayers.

GSTR 9B: It is the summary of TCS (Tax Collected at Source) filed in GSTR-8 by taxpayers registered as E-commerce operators under GST. GSTR-9B must be filed by the 31 of December following the end of a financial year. E.g., the due date for filing GSTR-9B for the financial year 2020-21 is 31 December 2022.

However, as the provision of section 52(TCS) is applicable from 01st October 2018 only, the E-commerce operators are not required to file GSTR-9B for the year 2017-18.

GSTR 9C: Form GSTR-9C is a return form required to be filed by registered taxpayers in case the aggregate turnover is more than Rs. 5 crores. In this case, the taxpayer has to also submit a copy of the audited annual accounts and reconciliation statement, reconciling the value of supplies declared in the return furnished for the financial year.

Note: Turnover of the complete year i.e. from 1st April 2017 to 31st March 2018 has to be taken into account for calculating the turnover. For example, if a taxpayer has a turnover of Rs. 5.1 Cr for the period 1st April 2017 to 31st March 2018 and a turnover of Rs. 1.9 Cr for the period 1st July 2017 to 31st March 2018, then the taxpayer is required to file form GSTR- 9C.

What is GSTR-9A and who has to file it?

GSTR-9A is a simplified GST annual return filed by business owners who have opted for the composition scheme under the GST regime. This return includes all the quarterly returns filed by the composite dealers in that financial year. This return is discontinued since the introduction of GSTR 4 (Annual).

What is GSTR-9B and who is liable to file it?

GSTR-9B is the summary of details filed in GSTR-8 by taxpayers registered as E-commerce operators under GST.

What is GSTR 9C and who has to file it?

Form GSTR-9C is a return form required to be filed by registered taxpayers in case the aggregate turnover is more than Rs.5 crores, whereas it is optional for taxpayers having turnover between 2cr to 5 cr. In this case, the taxpayer has to also submit a copy of audited annual accounts and reconciliation statement, reconciling the value of supplies declared in the return furnished for the financial year.

What is the penalty for not filing the GST Annual Return (GSTR-9) by taxpayers whom it may be liable to?

As per Section 47(2) of Central Goods and Service Tax Act (2017), a person will be fined a penalty of INR 100 per day (CGST) + INR 100 per day (SGST), amounting to a total of INR 200 per day if he/she fails to file GSTR-9 before the due date. However, the maximum amount of penalty a person can be fined is 0.25% of the total turnover.

When is the due-date for filing GSTR 9?

The due date for filing GSTR 9 is 31st December of the subsequent financial year. For example, the due date for filing GSTR-9 for the financial year 2021-2022 is 31st December 2022.

Here is a chronological explanation of all the extensions of GSTR 9 due date over the year.

FY 2017-18 Due Date(the period from 01.07.2017 to 31.03.2018)

- 22 Dec 2018: The due date for filing GSTR 9, GSTR 9A and GSTR 9C extended upto June 30, 2019 in the 31st GST Council Meeting held on December 22, 2018.

- 21 June 2019: The due date for filing GSTR 9, GSTR 9A and GSTR 9C extended upto August 31 , 2019 in the 35th GST Council Meeting held on June 21, 2019.

- 26th August 2019: The finance ministry extended the last date for GSTR 9 Filing by three months to November 30 from 31st August 2019.

- 3rd Feb 2020: The due date for GSTR-9 /GSTR-9C for FY 2017-2018 (the period from 01.07.2017 to 31.03.2018) was extended state-wise to 5th and 7th Feb 2020 via GST Notification 06/2020 dated 03-02-2020

FY 2018-19 Due Date

- 23rd Mar 2020: Extends the time limit for furnishing of the annual return for the financial year 2018-2019 until 30 June 2020 vide GST Notification 15/2020 dated 23-03-2020

- 5th May 2020: The GST annual return (GSTR-9) due date was further extended to 30th September 2020 via GST Notification 41/2020 dated 05-05-2020

- 30th Sep 2020: The GSTR-9 due date was further extended to 31st October 2020 via GST Notification 69/2020 dated 30-09-2020

- 28th Oct 2020: The date was further extended to 31st December 2020 for FY 2018-19 via GST Notification 80/2020 dated 28-10-2020

- 30 Dec 2020: Due date of GSTR 9, 9A & 9C for FY 2019- 20 is extended to 28th Feb 2021. However, due date for FY 2018-19 remains to be 31st Dec 2020 as per GST Notification 95/2020 dated 30th December 2020

FY 2019-20 Due Date

- Due date for furnishing GSTR 9 for the financial year 2019-20 was extended till 28 Feb 2021 as per GST Notification 95/2020 dated 30th December 2020

- CBIC extended the due date of GSTR 9 & 9C for FY 2019-20 to 31st March 2021 via GST Notification 04/2021

FY 2020-21 Due Date

- CBIC extended the due date of GSTR 9 & 9C for FY 2020-21 from 31st December 2021 to 28th February 2022 via GST Notification 40/2021

FY 2021-22 Due Date – 31st December 2022

GST ANNUAL RETURNS

Consequence of non-filing or failure to submit the annual return

One or more of the following can be the consequences of not filing Annual return

- Receipt of notice u/s 46 to file the return within 15 days.

- Late fee for non-filing or filing after due date shall be applicable u/s 47(2), being lower of

- Rs.100 per day during which such failure continues or

- 0.25% of turnover in the state or union territory.

- Note: The same late fee would also be applicable for SGST, whereby the total penalty for the registered person will be double the above amount.

- General penalty up to Rs.25,000 could be applicable as per section 125 of the Act.

Any Exceptions To The Filing Of Annual Return

There is no requirement to file the Annual Return by –

- An Input Service Distributor (ISD)

- A person paying tax under section 51 or section 52 (TDS / TCS)

- A casual taxable person and (CTP)

- A non-resident taxable person (NRTP)

Forms for filing the Annual Returns

Rule 80 of the CGST Rules lays down the manner in which Annual Return is required to be filed by the registered persons.

Every registered person who is required to file Annual Return under section 44 shall file it electronically in FORM GSTR-9 through the common portal.

In case of a person paying tax under composition scheme under section 10, the Annual Return has to be filed in Formb FORM GSTR-9A

E-commerce operator who is required to collect the tax under section 52 shall file Annual Return in the Form GSTR-9B .

Documents That Need To Be Submitted Along With The Annual Returns

The requirement to submit documents does not depend upon the filing of Annual Returns. Rather, it is linked to the applicability of getting your accounts audited. In GST liability for audit is governed by section 35(5) of the CGST Act 2017. As per the section, every registered person whose turnover during the financial year exceeds Rs 2 crore shall get his books of accounts audited.

Further, as per Section 44 (2) of the Act, every person who is required to get his accounts audited shall furnish the Annual Return along with the following documents-

Copy of audited annual accounts and

A Reconciliation Statement reconciling the value of supplies declared in the return furnished for the financial year with the audited annual financial statement, and such other particulars as may be prescribed.

How TaxAbide Helps

Assistance in downloading the desired forms GSTR-1, 2A, 2B, and 3B and comparing them with books of accounts to check mismatches.

Audit trail of GSTR-9\9C to GSTR-1, 2A, and 3B at the invoice level

Preparation of a Checklist to identify mismatches & compute the net tax payable.

Provide technical assistance and representative services during departmental audits.

Preparation and filing of annual returns through FORM GSTR-9 & 9C.