Form 16

Form 16

Form 16

Form 16 is a certificate issued under section 203 of the Income Tax Act, 1961, to salaried employees by their employers. Every month TDS is deducted from the salary income. Form 16 gives a detailed summary of the salary paid to the employee, the tax deducted at source (TDS) on the salary and deposited with the government by the employer.

Form 16 is a certificate issued to salaried employees by their employer that provides a detailed summary of TDS deducted and deposited to the Income tax authorities. Form 16 is an important document issued under the Income Tax Act of 1961 provisions.

Each salaried employee can obtain Form 16 from the employer on or before the 15th of June of the following year, immediately after the financial year in which the tax is deducted. If any employer delays or fails to issue Form 16 by the specified date, he is liable to pay a penalty of Rs.100 per day until the default continues.

Key Points About Form 16

Form 16 is a TDS certificate issued by employers to salaried employees. It contains details of salary paid and tax deducted at source during the financial year.

Issuance of Form 16

Employers are required to issue Form 16 to salaried employees on or before 15th June of the assessment year for which the income tax return is being filed.

Example: For FY 2022-23 (AY 2023-24), Form 16 should be issued by 15th June 2023.

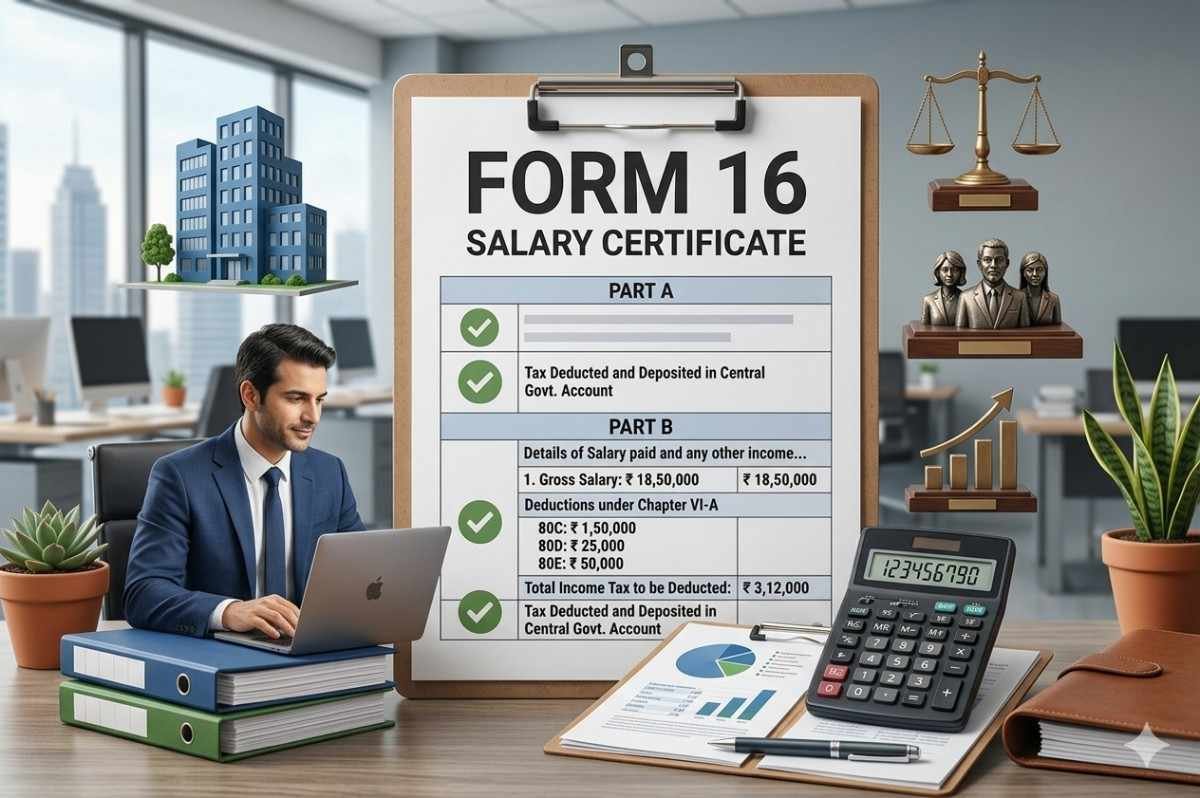

Components of Form 16

Form 16 consists of two parts – Part A and Part B.

Part A

Part A contains:

Employer and employee PAN details

Employer TAN details

Summary of TDS deducted and deposited

Other relevant tax details

Part B

Part B provides:

Salary breakup

Allowances and deductions under Section 80C, 80D, etc.

Taxable income details

Income from other sources, if any

Importance & Use of Form 16

Form 16 serves as a vital document for salaried individuals while filing income tax returns.

It helps employees:

Verify salary and TDS details

Calculate taxable income accurately

Claim deductions and exemptions

Reconcile taxes deducted by employer

File income tax return easily

Verification of Form 16

Employees should cross-verify the details mentioned in Form 16 with:

Salary slips

Bank statements

Form 26AS

Any mismatch should be immediately informed to the employer for correction.

Why Form 16 is Required

Form 16 is important because:

It acts as proof that tax deducted by employer has been deposited with the government

It helps in filing income tax return

It serves as proof of salary income

Banks and financial institutions require Form 16 while processing loans

Eligibility Criteria for Form 16

Every salaried employee whose income falls under the taxable band is eligible for Form 16.

If an employee’s income is below the taxable limit, TDS is not required to be deducted and the employer may not issue Form 16.

However, many organizations still provide Form 16 as a good practice because it gives a consolidated view of earnings and deductions.

Types of Form 16

Form 16

Form 16 is issued for TDS deducted on salary income by employers.

Form 16A

Form 16A is issued for TDS deducted on income other than salary such as:

Fixed deposit interest

Rent receipts

Insurance commission

Professional or contractual payments

It contains details of deductor, deductee, PAN, TAN, income details and TDS deposited.

Form 16B

Form 16B is issued for TDS deducted on sale of immovable property.

The buyer deducts 1% TDS on property purchase and deposits it with the Income Tax Department.

How to Download Form 16

Form 16 can only be downloaded and issued by the employer.

Individuals cannot download Form 16 themselves from the TRACES website using PAN number.

If an employer deducts TDS from salary, issuing Form 16 is mandatory.

Employers should issue Form 16 before the due date every financial year.

Rectify Mismatch in Form 16 & Form 26AS

If there is a mismatch between Form 16 and Form 26AS, follow these steps:

Contact your employer and inform them about the mismatch

Share supporting documents and discrepancy details

Request revised Form 16

Wait for updated details to reflect in Form 26AS

Cross-verify both documents before filing return

Is Form 16 and Form 16A Similar?

Form 16 and Form 16A are different documents though both are TDS certificates.

Form 16 is issued for salary income, while Form 16A is issued for non-salary income.

Consultants, professionals and individuals earning interest income or commission generally receive Form 16A.

Due Date for Issuing Form 16

Form 16 must be issued every year on or before 31st May for the financial year in which tax was deducted.

Due Dates for Form 16A

April – June : 15th August

July – September : 15th November

October – December : 15th February

January – March : 15th April